There are dozens of choices when it comes to budget plans. If you're still looking, or are completely new to the concept of budgeting, let me re-introduce you to an age-old budgeting guideline: the 50/20/30 rule. Even though it's a classic, it bears a fresh look, especially through the lens of the modern American's financial outlook.

Three Categories and What They Contain

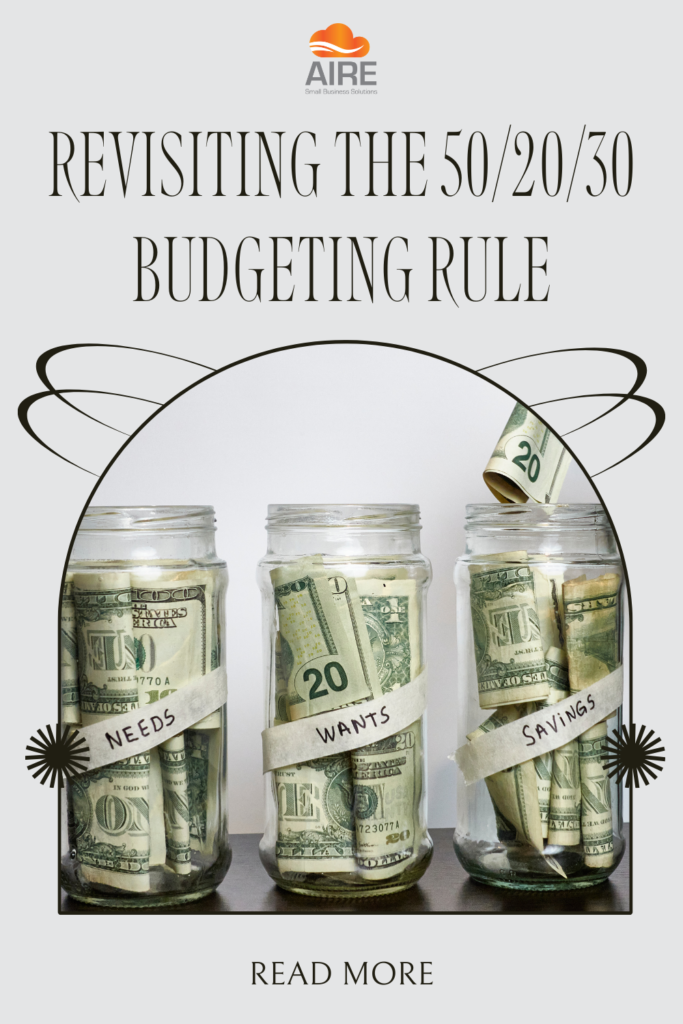

The 50/20/30 rule splits up take-home pay into three large spending categories — fixed costs, financial goals, and flexible spending. Here's a list of what each contains.

- Fixed Costs (50%) – These are the expenses most vital to your survival, which don’t vary from month to month: mortgage, rent, vehicle payment and utilities. Some versions also include non-essential monthly subscriptions, since they require a monthly commitment and the amount doesn’t vary unless you choose to discontinue them.

- Financial Goals (20%) – This category includes any monthly payments and contributions toward improved financial health: 401K and other retirement accounts (from post-taxed income), extra payments on credit card debt or student loans, building an emergency fund, and savings goals such as a down payment for a home or funding an education.

- Flexible Spending (30%) – This category includes expenses that vary from month to month: groceries, gas, eating out, shopping, hobbies and entertainment.

Some Pros, Some Cons

One of the best traits of the 50/20/30 guideline is its simplicity. There aren't dozens of categories to micromanage, but it will still get the job done. This is a great starting point for everyone, especially if you've never stopped to look at the bigger picture of your spending balance.

Nonetheless, the plan may not work for everyone. Keeping fixed costs under 50% and saving 20% might be unreachable to many people in their present circumstances. On the other hand, some advisors think the plan should be more like 50/30/20 – saving more and leaving less for flexible spending. For that matter, choosing a more minimalist approach to living (smaller house, older cars) can reduce fixed costs well below 50%, especially among those with higher-than-average incomes. However you choose to view it, the 50/20/30 rule is best described not as a strict budget, but a helpful guideline.

How to Use 50/20/30 in Today's Financial Landscape

Reduce Your Fixed Costs

Financial experts recommend your fixed living costs not exceed 50% of your income, but — thanks to huge mortgages, multiple vehicles, and skyrocketing rent — many Americans will find themselves over this amount. Know what percentage of your income is consumed by fixed expenses, then identify ways to reduce them: refinance your home, negotiate lower interest rates, or choose not to buy new vehicles every few years. If you include subscriptions in this category, see how many can be reduced or eliminated – magazines, movie clubs, cable or satellite, Internet, data plans, gym memberships.

Look for Ways to Spend More on Your Financial Goals

Reducing your fixed costs will allow you to designate more income toward your savings and other financial goals. Maybe you're barely saving 5% right now, but even small changes can make a difference. In our debt-burdened society, it can also be difficult to choose between paying off debt and saving for retirement, especially when you're young and retirement is still far away. Remember that the more you contribute to retirement accounts when you're young (both pre and post-tax), the more it will compound (that also goes for high-yield savings accounts). Even if your current focus is debt, continue to contribute as much as you can to retirement and savings. When you eliminate bad debt, use former payment funds to increase your retirement and savings contributions.

Be More Controlling with Flexible Spending

You may never be able to completely predict all the categories under flex spending, but the more you can control, the closer you'll get to flip-flopping that 30% with 20% and save more for future goals by spending less on immediate wants. Try limiting how much you eat out or go to the movies, and take advantage of rewards cards, fuel points, coupons, and rebates to reduce your grocery and gas bill on a regular basis.

It may be basic, but if you follow these tips, the 50/20/30 rule might just be the tool that helps you get out of debt and improve your financial outlook for good.

Written by Jessica Sommerfield for MoneyNing and legally licensed through the Matcha publisher network. Please direct all licensing questions to legal@getmatcha.com.